Table of Content

In most cases, you can’t withdraw money from your tax-advantaged retirement accounts without penalty until you turn age 59 ½. Avoid using your Roth IRA for a home purchase if you’re behind on retirement savings. That may mean you need to save up longer to buy a home, but being patient is worth it so you don’t jeopardize your golden years. You should also think twice if you may need the Roth IRA for your child’s college education, given that you can also avoid the early withdrawal penalty if you use the funds to pay for higher education. While Roth IRAs are designed primarily for retirement savings, you can also withdraw up to $10,000 of your account’s earnings for a first-time home purchase. You can also use that money to build or rebuild a first home.

When money is withdrawn from the Roth IRA, the potential for additional growth is eliminated, as is the opportunity to benefit from compounding interest. Even if you have owned a home in the past, you may still be able to qualify as a first time home buyer and withdraw money from your Roth IRA. You can withdraw from the contributions you have made into your Roth IRA at any time, for any reason. There is no tax or penalty, and you can use the money however you like.

Things to Consider Before Withdrawing from Your Roth IRA

590-A for more information on ways to get a waiver of the 60-day rollover requirement. For purposes of Form 5329, a traditional IRA is any IRA, including a simplified employee pension IRA, other than a SIMPLE IRA or Roth IRA. For the latest information about developments related to Form 5329 and its instructions, such as legislation enacted after they were published, go to IRS.gov/Form5329. We neither keep nor share your information entered on this form.

Enter the excess of your contributions to Roth IRAs for 2022 (unless withdrawn—discussed below) over your contribution limit for Roth IRAs. See the instructions for line 19, earlier, to figure your contribution limit for Roth IRAs. The additional tax doesn’t apply to the distributions that are includible in income described next. Enter on line 6 the amount from line 5 that you can exclude.

Can I use my Roth IRA for a first time home purchase?

They will be able to see your return and guide you to completion. To access that service please follow the instructions below. Yes, I entered information for the Roth conversion in 2020, and also the "contributions prior to 2021" screens. I was a little confused by these screens, but did the best I could with the documents that I have available. It must be used to payqualified acquisition costsbefore the close of the 120th day after the day you received it.

On one hand, if you start saving early for retirement, your money has more time to grow with compound interest. On the other hand, saving for a down payment on a home in today’s market can take years depending upon the purchase price and loan program you choose. According to research by Zillow, it takes about seven years for home buyers to save a 20% down payment for the median value of a home in the U.S. Don’t include ABLE rollovers or program-to-program transfers in figuring your excess contributions. If the contributions to your ABLE account for 2022 were more than is allowable, you may owe tax on the net income resulting from the excess contribution. Enter the difference, if any, of your contribution limit for traditional IRAs less your contributions to traditional IRAs and Roth IRAs for 2022.

Should You Use Your Roth IRA to Buy Your First Home?

In the long run, you’d find yourself closer to financial wellness. Purchasing your own home is probably one of the biggest investments you’ll ever make. If you’ve been saving for retirement, it’s tempting to raid your Roth IRA for the down payment or to cover closing costs. Taking money from your Roth IRA now, even if you won’t face an early-withdrawal penalty, means you take two hits. First, you shave off a chunk of what you’ve already saved and is growing tax-free.

Part I—Additional Tax on Early DistributionsLine 1Distributions from a designated Roth account.Recapture amount subject to the additional tax on early distributions. It appears you do not qualify to put the money back within the rollover period or the delay exception period. However, if you have not made your ROTH IRA contribution for 2021 you could contribute up to the maximum amount allowable . Reply to this if you need clarification or additional information. The funds must be used within 120 days from the date the distribution is received.

How can I withdraw money from my Roth IRA without penalty?

"and used the total distribution for purchase of a first home." Bankrate follows a strict editorial policy, so you can trust that our content is honest and accurate. The content created by our editorial staff is objective, factual, and not influenced by our advertisers. Bankrate has partnerships with issuers including, but not limited to, American Express, Bank of America, Capital One, Chase, Citi and Discover.

A qualified first-time homebuyer distribution from line 20 of your 2022 Form 8606. Also include this amount on line 2 and enter exception number 09. If you received an early distribution from your designated Roth account, include on line 1 the amount of the distribution that you must include in your income. You will find this amount in box 2a of your 2022 Form 1099-R. You may also need to include a recapture amount on line 1 if you have ever made an in-plan Roth rollover . See the instructions for line 2, later, for other distributions that aren’t subject to the additional tax.

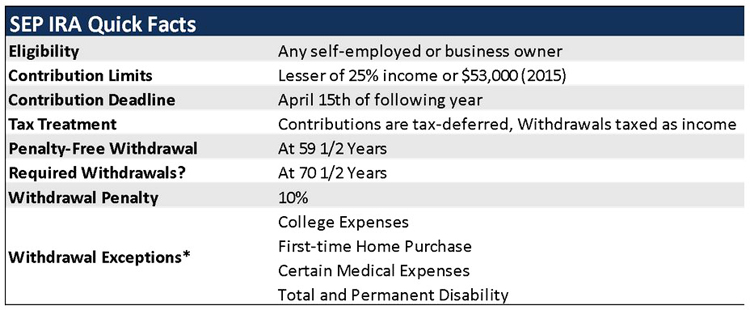

And don't forget, the term real estate doesn’t refer only to property. You can invest in vacant lots, parking lots, mobile homes, apartments, multifamily buildings, and boat slips. You can tap into your IRA and qualify for the exemption if the money is to help an eligible child, grandchild, or parent buy a home.

If the contributions to your Coverdell ESAs for 2022 were more than is allowable or you had an amount on line 33 of your 2021 Form 5329, you may owe this tax. You contributed $1,000 to a Roth IRA in 2020, your only contribution to Roth IRAs. In 2022, you discovered you weren’t eligible to contribute to a Roth IRA in 2020. On September 7, 2022, you withdrew $800, the entire balance in the Roth IRA. You must file Form 5329 for 2020 and 2021 to pay the additional taxes for those years. When you complete Form 5329 for 2022, you enter $1,000 (not $800) on line 20 because you withdrew the entire balance.

Other qualifying exemptions include medical costs, tuition, payments to prevent eviction, funeral expenses, and damage to a principal residence. Enter the excess of your contributions to traditional IRAs for 2022 (unless withdrawn—discussed next) over your contribution limit for traditional IRAs. See the instructions for line 10, earlier, to figure your contribution limit for traditional IRAs. Don’t include rollovers in figuring your excess contributions.

Withdrawals of earnings not meeting both of these criteria are subject to tax and penalties. IRA withdrawal rules allow you to take money penalty-free for qualified higher education expenses. It’s essential that you’re able to continue saving for retirement once you’ve bought your first home. With a Roth IRA, you can avoid both taxes and penalties when withdrawing up to $10,000 of earnings to buy your first home if you’ve had the account for five years.

In a perfect scenario, you wouldn’t choose to become a homeowner at the expense of draining your retirement nest egg. Instead, explore other options such as opening a Roth IRA and treat it almost like a savings account, with the intention of using it for your first home purchase five years from now. Keep market conditions in mind and compare your mortgage interest rate to the expected long term return you would earn by keeping your money in your Roth IRA. Although using money from your Roth IRA may seem like an easy source to fund a down payment to purchase your first home, it might not be the right decision for everyone. Before you cash out your Roth IRA, think about how it might broadly impact your financial future. After five years, you can withdraw all of your contributions and up to $10,000 of your investment earnings—but you might not have earned that much yet.

And what if you don’t end up buying a home, or you come up with another source of down payment? A Roth IRA is still a win, since you can leave that money be and let it continue to grow for your retirement. Because this withdrawal benefit is available only once in a lifetime, ideally, you might want to time it so that you only tap into your Roth after you’ve earned the full amount allowable. Here are a few reasons you may consider leveraging a Roth IRA to become a first-time homeowner without having to delay your retirement goals, and some tips on how to go about it. While you’ve probably been told that you should never tap into your retirement money, using cash from a Roth IRA to fast-track your dream of home ownership can be a worthy exception.

No comments:

Post a Comment